Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Second Chance Home Buyers Program in North Carolina: How to Buy a Home Even After Setbacks

If you’ve been told “no” before, because of credit, a past foreclosure, or a bankruptcy. Here’s the truth:

👉 You may still be able to buy a home in North Carolina.

I work with buyers across Western North Carolina and Haywood County, and I’ve seen firsthand how many people qualify for what I call a “second chance” at homeownership, even when they thought it wasn’t possible.

Whether you’re trying again after being denied or planning on relocating to Western North Carolina, understanding your options (and your credit score) is the key to moving forward.

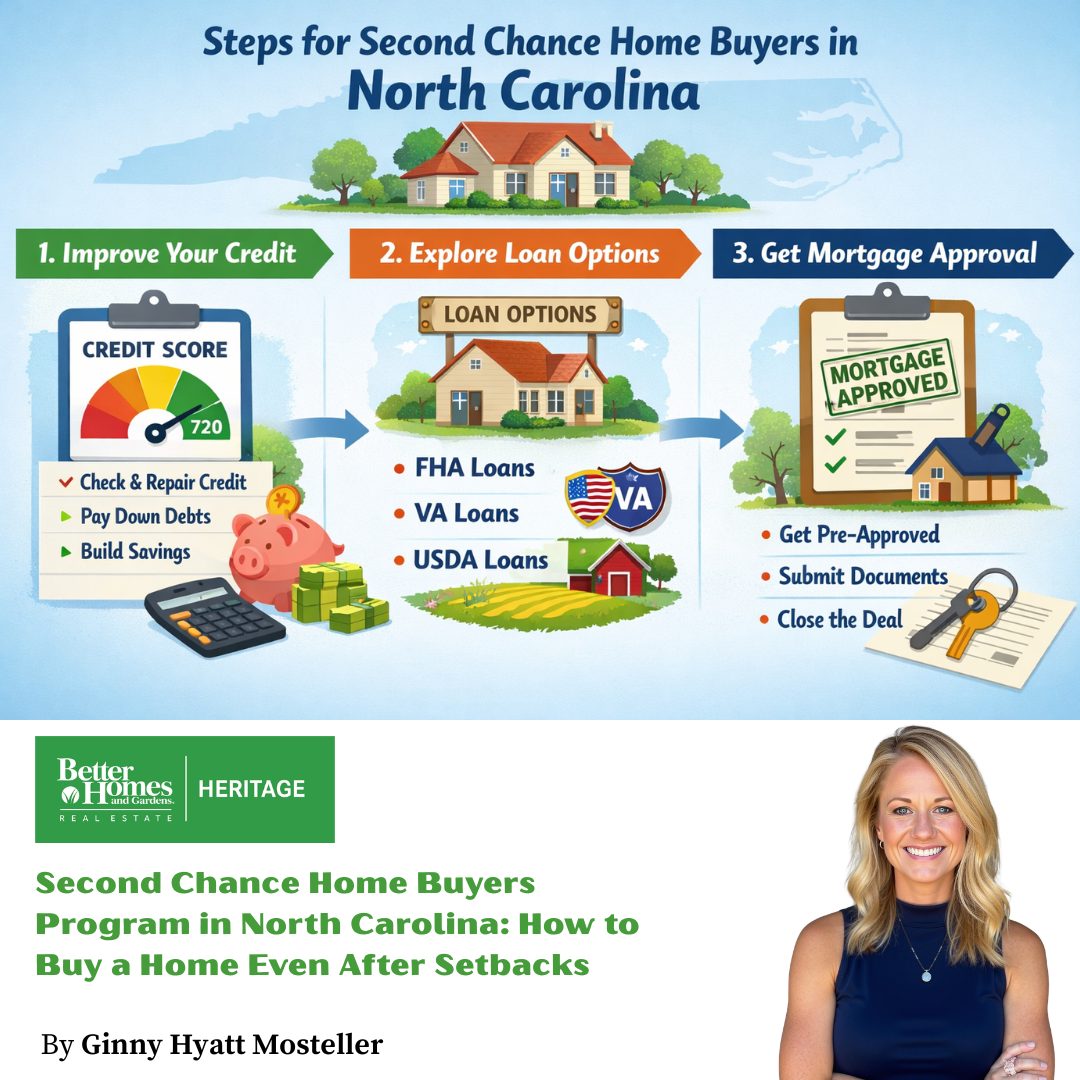

What Is a Second Chance Home Buyers Program?

A “second chance home buyers program” isn’t always one specific program, it’s a combination of:

- Flexible loan options

- Credit-friendly guidelines

- Down payment assistance programs

These are designed to help buyers who:

- Have lower credit scores

- Went through foreclosure or bankruptcy

- Were previously denied by a lender

- Are rebuilding financially

👉 The biggest factor? Your first-time home buyer credit score NC and how lenders view your current financial picture.

What Credit Score Do You Need for a Second Chance in NC?

Let’s break this down clearly:

Realistic Credit Score Ranges in North Carolina

- 580+ → FHA loan eligibility (most common “second chance” option)

- 620+ → Conventional loan minimum

- Many lenders use 640 as a common benchmark for USDA loans, though USDA does not publish one universal minimum score for every lender.

- 580–620 → Many buyers still qualify with the right lender

In my experience, I’ve helped buyers:

- Get approved after being denied elsewhere

- Qualify with scores in the 580–600 range

- Improve their score quickly and unlock better options

👉 If you’re asking, “can I buy a house in NC with bad credit?” The answer is often YES.

Waiting Periods After Financial Setbacks

One of the biggest myths is that you have to wait forever. That’s not true.

Typical Waiting Periods in NC

- Chapter 7 Bankruptcy: 2 years (FHA)

- Some buyers may qualify during a Chapter 13 repayment plan with court and lender approval, depending on the loan program and circumstances.

- FHA waiting periods after foreclosure are commonly around 3 years, though exceptions and lender overlays can apply.

- Short Sale: 2–4 years

- Late Payments / Collections: No set timeline (case-by-case)

I’ve worked with buyers in Haywood County NC real estate who thought they needed 5–7 years, but were actually eligible much sooner.

Best Loan Options for Second Chance Buyers

Not all loans are created equal — especially for second-chance buyers.

1. FHA Loans (Most Common)

- Credit score: 580+

- Low down payment (3.5%)

- Flexible credit guidelines

👉 This is often the best path forward for buyers rebuilding credit.

2. USDA Loans (Great for WNC Buyers)

- Credit score: ~640 typical

- 0% down payment

- Available in many rural areas

This is huge if you’re looking at WNC mountain homes with views or properties outside city limits.

3. Conventional Loans

- Credit score: 620+

- Better rates at higher scores

- Stricter approval

If your score improves, this can become a strong option.

Real Examples From My Experience

This is where things get real.

In my work with buyers across Western North Carolina, I’ve seen:

- A buyer denied by one lender get approved by another with a 580 score

- A client post-bankruptcy qualify in just over 2 years

- Buyers raise their score 30+ points in a month with the right strategy

- Renters transition into owning mountain homes for sale in Western North Carolina they didn’t think were possible

👉 The biggest mistake I see? Waiting too long to start the conversation.

How to Improve Your Chances Quickly

If you’re close but not quite ready, here’s what I recommend:

- Pay down credit cards below 30% utilization

- Avoid opening new accounts

- Make every payment on time

- Work with a lender who offers rapid rescore

- Get pre-qualified early (even if you’re not ready yet)

Why Credit Score Matters More Than You Think

Your first-time home buyer credit score NC impacts:

- Your loan approval

- Your interest rate

- Your monthly payment

- Your overall buying power

Even a small increase in your score can mean thousands saved over time.

Local Advantage: Western North Carolina Opportunities

If you’re considering a second chance at buying, location matters.

In areas like Haywood County:

- USDA loans are widely available

- Home prices can offer more value vs larger metros

- You can find incredible mountain homes with views

Whether you’re local or relocating to Western North Carolina, this market offers real opportunity, especially for buyers starting over.

Frequently Asked Questions

Can I buy a house in NC with bad credit?

Yes. Many buyers qualify with scores as low as 580, especially using FHA loans.

What is the minimum credit score for conventional loan NC?

Most lenders require at least 620, but better terms start around 680+.

How long after bankruptcy can I buy a house in NC?

Typically 2 years for FHA loans, sometimes sooner depending on the situation.

Are there programs for first-time home buyer North Carolina?

Yes! Including down payment assistance and flexible loan programs designed for first-time buyers.

What is the fastest way to qualify again?

Work with a local expert, improve your credit strategically, and get pre-qualified early.

Ready for Your Second Chance?

If you’ve been waiting, wondering, or told “not yet”. This is your sign to take the next step.

Whether you’re searching for:

- Haywood County NC real estate

- Mountain homes for sale in Western North Carolina

- Or planning on relocating to Western North Carolina

👉 I can help you understand where you stand and what your next move should be.

Send me a message today! Your second chance might be closer than you think.